Chester Cheung is the Content Marketing Specialist for the Hong Kong market at Sleek, crafting localized, high-conversion bilingual content that empowers entrepreneurs to make confident business decisions.

Drawing on a background in finance and digital marketing, including roles at HSBC and in the digital agency space, Chester combines commercial rigor and performance-driven storytelling to every piece he ships. His focus is on translating complex business and compliance concepts into clear, actionable insights for busy founders.

Having worked across both structured corporate environments and agile teams, Chester knows what business owners value most: reliable information without the jargon. At Sleek, he leverages this perspective to produce insightful, accessible content that drives customer acquisition and fosters long-term value.

When he’s not writing, Chester is an active runner and an amateur photographer.

Before day one: Written employment contract + Employees' Compensation insurance.

Within 60 days: Enrol them in MPF (you and they each pay 5%, capped at HK$1,500/month).

Every month: Run payroll, issue payslips, file IR56 forms (IR56E, then annual BIR56A/IR56B).

Minimum pay: HK$43.1/hour from 1 May 2026, plus statutory leave.

Hiring your first employee in Hong Kong is a milestone, and the point where a founder suddenly has real compliance obligations. Most people worry they’ll miss something and land a penalty. The good news is the rules are clear and the list is short.

There are three things to get right: a written employment contract, MPF enrolment, and a payroll process, plus the statutory rights every employee is owed. None of it is complicated once you know the steps.

In this guide, you’ll learn:

What to prepare before your first employee starts

What to include in a Hong Kong employment contract

How MPF enrolment and contributions work

How to handle payroll, payslips, and IR56 forms

What statutory entitlements apply to a first hire

What do you need before hiring your first employee?

Before your first employee starts, you usually need three things in place: a written employment contract, Employees’ Compensation insurance, and access to an MPF scheme for enrolment. Two of these have clear legal deadlines once employment begins, so it is easier to set them up before day one.

Your core pre-hire tasks are:

Employment contract: Put the main terms in writing before the start date.

MPF scheme: Set up an MPF scheme with a trustee so you can enrol the employee within the statutory deadline.

Employees’ Compensation insurance: Arrange a valid policy that covers work injury and occupational disease from the first day of employment.

Record-keeping process: Be ready to keep payroll and MPF records from day one and retain them for at least seven years.

If you are engaging a genuine freelancer instead of an employee, the rules may be different. But classification matters: if someone is really working as an employee, treating them as an independent contractor can create compliance risk.

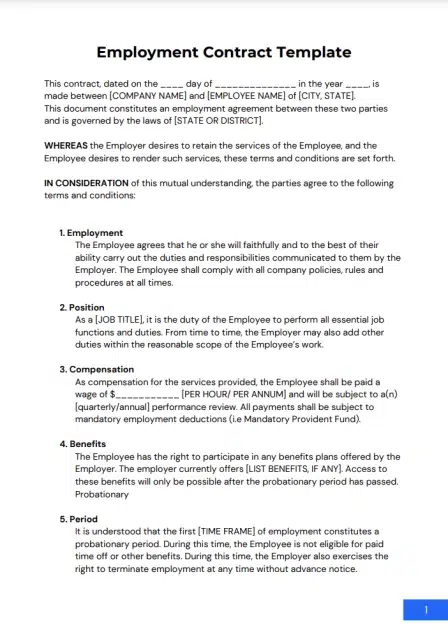

What should a Hong Kong employment contract include?

Template of a Hong Kong Employment Contract

A Hong Kong employment contract should clearly set out pay, wage period, duties, working hours, leave, notice, and MPF arrangements. A verbal agreement may be legally possible in some cases, but a written contract is the safer and more practical approach for both sides.

At a minimum, the contract should cover:

Job title and duties: What the employee does and who they report to

Wages and wage period: Salary, payment date, and the wage period covered

Working hours and rest days: Expected hours and rest-day arrangement

Probation period: If used, how long it lasts and what notice applies during probation

Leave entitlements: Annual leave, statutory holidays, sick leave, and any extra contractual leave

Notice period: What either side must give on termination

MPF arrangement: Confirmation that the employee will be enrolled under the statutory rules

Need a starting point? Download our employment contract template and adapt it to your role. It covers the essential terms above so you’re not drafting from scratch.

How does MPF enrolment work for a first hire?

The Mandatory Provident Fund (MPF) is Hong Kong’s compulsory retirement-savings scheme. As the employer, you pick a scheme, enrol your employee, and pay contributions every month.

If an employee is aged 18 to 64 and employed for a continuous period of 60 days or more, the employer must enrol them in an MPF scheme within 60 days of their first day.

Here is how the contributions work in 2026:

Monthly relevant income

Employer contribution

Employee contribution

Below HK$7,100

5% of income

Nothing (employee exempt)

HK$7,100 to HK$30,000

5% of income

5% of income

Above HK$30,000

HK$1,500 (capped)

HK$1,500 (capped)

A few practical points for a first hire:

Employer contributions start from day one of employment, even though the employee’s own contributions have a 30-day holiday at the start.

Contributions are due by the contribution day each month (generally the 10th of the following month).

Foreign employees on an employment visa of 13 months or less, or already covered by an overseas retirement scheme, may be exempt.

Missing the 60-day deadline is a criminal offence under the MPF Schemes Ordinance, so build enrolment into your onboarding from the start.

You can also make extra MPF contributions voluntarily, and you should be aware that the rules on using MPF to offset severance and long-service payments have changed (see MPF offset changes), so you can no longer reduce those payments with your MPF contributions.

Tip

Don't let the 60-day clock catch you out. You must enrol an eligible employee in MPF within 60 calendar days of their first day, including holidays, and the probation period counts. Miss it and you're not just late, you've committed an offence under the MPF Schemes Ordinance. Set a reminder at the start date, or have your payroll provider track it for you.

How do I set up payroll for my first employee?

Setting up payroll means calculating each pay cycle (salary, deductions, and MPF), issuing an itemised payslip, paying on time, and filing the right IR56 forms with the Inland Revenue Department. For a new employer, the form that matters first is the IR56E.

The recurring monthly cycle is straightforward once it is set up:

Calculate pay. Gross salary, less any authorised deductions, plus allowances or approved expense claims.

Calculate MPF. 5% employer and 5% employee within the income limits above.

Issue a payslip. Itemised, showing wages, deductions, and contributions.

Pay on time. Within seven days of the end of the wage period.

Submit MPF. File and pay the monthly MPF contribution by the contribution day.

IR56E: notify the IRD within three months of hiring a new employee.

BIR56A with IR56B: the annual Employer’s Return, filed each year for the 1 April to 31 March tax year, with an IR56B completed for each employee.

IR56F or IR56G: filed when an employee leaves or departs Hong Kong.

Getting payroll right from the first hire saves rework later, because clean records feed straight into your year-end accounting services and Profits Tax filing.

What statutory entitlements must I provide?

Hong Kong employees on a continuous contract are entitled to paid annual leave, statutory holidays, rest days, sick leave, and, where applicable, maternity or paternity leave. You must also pay at least the statutory minimum wage and hold Employees’ Compensation insurance. These are floors set by the Employment Ordinance, not optional benefits.

The core entitlements for a typical full-time first hire:

Minimum wage: At least HK$43.1 per hour from 1 May 2026. Where an employee earns below HK$17,600 per month, you must record their total hours worked.

Rest days: At least one in every seven days for employees on a continuous contract.

Statutory holidays: Paid statutory holidays as set each year (the number increased in recent years as statutory and general holidays were aligned).

Annual leave: Paid annual leave starting at seven days and rising with years of service.

Sick leave: Paid sickness days accumulate with service, paid at four-fifths of normal wages when conditions are met.

Maternity and paternity leave: Paid leave for eligible employees under the Employment Ordinance.

Because several entitlements scale with service length or may change over time, it is worth checking the latest Labour Department guidance before finalising the contract and offer letter.

Common mistakes when hiring a first employee

Assuming one employee is too small for formal payroll

A common mistake is thinking payroll only matters once a business has several staff. In practice, the same core obligations start from the first salaried hire, including payslips, MPF, record-keeping, and IR56 reporting.

Waiting until after the start date to sort MPF

MPF has a statutory enrolment deadline, and employer contributions start from day one. Leaving setup too late is one of the easiest ways for a first-time employer to create avoidable compliance problems.

Treating an employee like a freelancer

Some founders try to keep things informal by calling the first hire a contractor. If the working relationship is really employment in substance, that label will not remove the underlying obligations.

Forgetting insurance from day one

Employees’ Compensation insurance is not optional and does not start only when the team grows. It applies from the first employee, regardless of hours worked.

When might in-house payroll be fine, and when might support help?

In-house payroll may be workable if:

You have one straightforward employee

Pay is fixed each month

You are comfortable tracking deadlines and filings

You already have accounting support internally

External support may help if:

You are hiring your first employee and want someone to manage the setup

You are unsure about MPF, IR56 forms, or statutory entitlements

You want payroll, bookkeeping, and tax records to stay aligned

You expect to add more employees soon

The right choice depends less on company size than on how much admin capacity and compliance confidence you already have.

How Sleek runs payroll and MPF for you

Your first hire is exciting. The admin behind it isn’t. Sleek takes the recurring compliance off your plate so you can focus on your new team member.

With Sleek, your first hire is handled end to end:

Onboarding the employee:Payroll profile setup, MPF enrolment, and the IR56E filing with the IRD.

Every month: Salary, deductions, and MPF calculated, itemised payslips issued, and the MPF e-submission filed on time.

Every year: The BIR56A Employer’s Return prepared and filed, with an IR56B for each employee.

One team: Payroll, bookkeeping, and tax filing under the same Hong Kong accountants, so salary costs flow straight into your books.

This matters most at the first hire, when the deadlines are unfamiliar and a missed MPF enrolment or late IR56E can mean penalties.

Ready to set up payroll for your first employee?

Sleek sets up the payroll profile, MPF enrolment, and IR56E filing for you.

FAQs about hiring your first employee in Hong Kong

Do I need to register as an employer before hiring?

You do not file a separate employer registration before hiring, but you must notify the IRD of the new employee by filing Form IR56E within three months of the start date. You also need an MPF scheme and Employees’ Compensation insurance in place. In practice, sort the insurance and MPF scheme before day one.

How soon must I enrol my first employee in MPF?

Within 60 days of their first day of employment, counted in calendar days including holidays. The employee’s probation period counts toward the 60 days. Your employer contributions start from day one, while the employee’s own 5% has a 30-day holiday at the start. Missing the deadline is a criminal offence under the MPF Schemes Ordinance.Realistically 8 to 16 weeks from a complete application, allowing for back-and-forth on documents. The biggest cause of delay is an incomplete application: missing financial projections, premises proof, or insurance. You cannot legally serve customers until the licence is issued, so plan your launch around the wait.

How much do MPF contributions cost me as an employer?

You contribute 5% of the employee’s relevant income each month, capped at HK$1,500 where they earn HK$30,000 or more. If they earn below HK$7,100 a month, you still pay your 5% but the employee is exempt from their share. Note the MPFA proposed raising these income thresholds in 2026, so the cap may change; verify before you budget.

Does Hong Kong deduct income tax from each pay cheque?

No. Hong Kong has no monthly tax withholding. You report what you pay your employee to the Inland Revenue Department, and your employee settles their own salaries tax directly. Your job is accurate reporting through the IR56 forms, not deducting tax each month.

What is the minimum wage in Hong Kong?

The statutory minimum wage is HK$43.1 per hour from 1 May 2026, up from HK$42.1. It applies to almost all employees regardless of contract type or pay frequency. A few categories, such as live-in domestic helpers, are exempt.

View more

Do I need payroll if I only have one employee, or none?

If you have no employees and pay yourself only through dividends or director fees, you do not need monthly payroll. The moment you hire one employee on a salary, payroll and MPF apply in full, with the same deadlines as a larger employer. There is no small-employer exemption from MPF or the IR56 filings.

What is a continuous contract, and why does it matter?

From 18 January 2026, an employee is on a continuous contract once they’ve worked at least 68 hours for you over any four-week period — the “468 rule”. It matters because most statutory entitlements, including paid annual leave, rest days, sickness allowance and severance, apply to employees on a continuous contract.

Do I need insurance to hire staff in Hong Kong?

Yes. Employees’ compensation insurance is a legal requirement as soon as you have employees, regardless of how many. It covers work-related injuries and illness. Trading without it is an offence under the Employees’ Compensation Ordinance.

Can Sleek handle MPF and payroll for my first hire?

Yes. Sleek’s payroll service sets up your employee’s payroll, enrols and submits their MPF, issues payslips, and files the IR56E and IR56B forms with the IRD. It’s built so first-time employers stay compliant without building an HR function.