Missing an IR56 form deadline can trigger costly penalties, and wrestling with every employer return only compounds the risk. Late fees escalate quickly, audits loom, and departures can stall at the airport. Each letter—E, F, B, M—has its checklist and clock. One wrong category or date sparks five-figure fines.

This guide slices through the red tape, giving you clear steps and foolproof timelines to file fast and stay compliant.

Don't risk any IR56 penalties

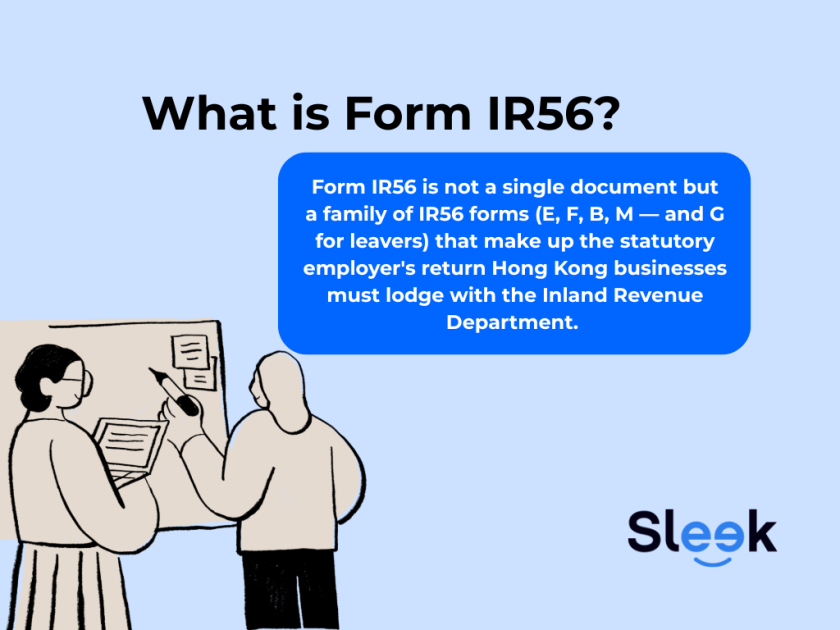

What is Form IR56?

Form IR56 is not a single document but a family of IR56 forms (E, F, B, M—and G for leavers) that make up the statutory employer’s return Hong Kong businesses must lodge with the Inland Revenue Department.

Together they record salaries, bonuses and other payments so the IRD can assess each worker’s Salaries Tax, and late or missing filings attract stiff penalties.

Form | Purpose | Who files | Deadline* |

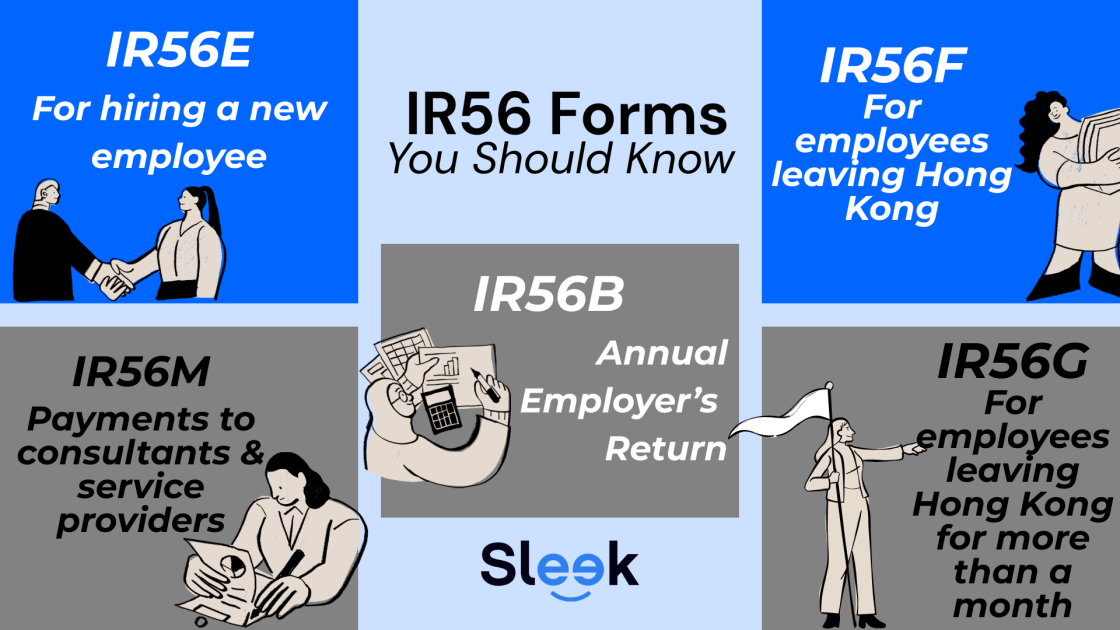

IR56E | Notify IRD of a new employee | Employer | Within 3 months of start date |

IR56F | Report an employee’s service ending (still in HK) | Employer | ≥ 1 month before cessation |

IR56B | Annual remuneration details for each employee | Employer | Within 1 month of IRD issuing BIR56A (usually early May) |

IR56M | Declare payments to non-employee local service providers (consultants, subcontractors, etc.) | Payer / Employer | With BIR56A & IR56B—i.e., within 1 month of April issue |

IR56G | Report cessation when an employee is leaving Hong Kong permanently or for > 1 month | Employer | ≥ 1 month before departure; withhold final pay until Letter of Release |

Important Note: Separate rules apply to IR56G for employees departing Hong Kong.

IR56E – For hiring a new employee

Use the IR56E Form whenever you onboard staff in Hong Kong. The form, also known as the IRD Form for New Employee, provides the IRD with a new hire’s start date, salary, and personal details to ensure their Salaries Tax record is opened correctly.

File it within three months of commencement as part of your broader IRD Employee Forms bundle.

Key fields cover:

- HKID/passport number

- Job title

- Salary package

- Employer File Number

Double-check them to avoid costly resubmissions. Submit via eTAX or post the signed hard copy.

IR56M – Payments to consultants & service providers

Use the IR56M Form, often labelled the 56M Tax Form or “56M IRD,” to declare fees paid to non-employees such as:

- Independent consultants working under a service contract

- Freelancers and subcontractors paid for ad-hoc projects

- Directors’ fees where no employment contract exists

Common mistakes to avoid when filing IR56M

- Treating true employees as contractors to skip MPF and tax reporting.

- Omitting travel, accommodation, or other reimbursed expenses that are part of the fee.

- Filing only at year-end—IR56M must accompany your annual Employer’s Return (BIR56A/IR56B) within one month of the IRD’s April issue date.

IR56B – Annual Employer’s Return

The IR56B Form is the backbone of your annual employer’s return, summarising every employee’s total pay for the tax year. IRD typically issues BIR56A + IR56B packages each April, and you have one month to file, so mark your calendar for early May.

Annual cycle

- April – IRD issues BIR56A/IR56B.

- May – Submit the completed IR56B (or IR56B Form 2025 in the current cycle).

- June–March – Keep payroll records ready for next year’s run.

Penalties to avoid

- HK$10,000 fine per late return.

- Daily default fines until submission.

- Possible prosecution for persistent non-compliance.

Submit on time, attach accurate schedules, and keep stamped copies to stay penalty-free.

IR56F – For employees leaving Hong Kong

When a staff member will cease employment yet remain in Hong Kong, you must file the IR56F Form (sometimes called the 56F Form) so the IRD can finalise that worker’s Salaries Tax via a 56F Tax Form assessment. Follow these steps to complete an IR56F form sample flawlessly:

- Collect details such as employee’s name, HKID/passport, last working day, and every dollar of remuneration up to cessation.

- Calculate final pay and include salary, allowances, bonuses, paid-out leave and benefits in kind.

- Fill Sections 1–12 and enter Employer File Number, personal particulars, dates and income figures; leave unused boxes blank.

- Sign and write the date. An authorised signatory must ink-sign before lodging.

- Submit ≥ 1 month before the last day – upload through eTAX or mail the original hard copy and keep a stamped copy for your records.

IR56G – For employees leaving Hong Kong for more than a month

Use IR56G when an employee will leave Hong Kong permanently or for more than a month. File the form with the IRD at least one month before departure and withhold all final payments until you receive a Letter of Release.

List the employee’s HKID or passport number, departure date, and full remuneration, then submit via eTAX or by post and keep a stamped copy to avoid penalties.

IR56F vs IR56G

IR56F applies when an employee stops working but remains in Hong Kong, while IR56G covers departures from Hong Kong. The table below highlights the key distinctions.

Aspect | IR56F | IR56G |

Purpose | Report cessation of employment when the employee will stay in Hong Kong | Report cessation when the employee will leave Hong Kong for good or for more than one month |

Filing deadline | File at least one month before the last working day | File at least one month before the departure date |

Payment withholding | Employer can pay all final sums once the form is lodged | Employer must withhold all final payments until the IRD issues a Letter of Release |

Common pitfalls | Filing IR56G by mistake or missing allowances in income total | Forgetting to withhold payments or understating benefits in kind |

How to file IRD forms online

Handling IRD online forms is straightforward once you know where to click. Follow these six steps.

- Sign in or register for eTAX and enter your TIN and password.

- Open the link titled “Filing of Employer’s Return / Notification” within the Business section to launch the employer menu.

- Choose your preferred filing mode by selecting Direct Keying to type forms on screen or Upload Data File if you prepared an IR56 Data File.

- Complete the form fields for IR56E, IR56F, IR56G, IR56B, or IR56M. The system prompts for HKID, salary figures, and dates, and hover tips explain how to fill each IRD Form box correctly.

- Review all entries, apply the authorised signer’s digital signature, press Submit, and save the PDF receipt for your records.

- Download an IRD Tax Return Sample from the IRD help page and compare it field by field before the deadline if you need reassurance.

Address, status, and payroll changes

Inform the IRD within one month whenever your company moves. File Form IR1249 or IRC3111A online through eTAX, send it by fax, or post it to the Commissioner of Inland Revenue to keep employer mail flowing. Prompt notice prevents missed returns and penalties, so add change of address inland revenue hk to every compliance checklist.

Turn IR56 compliance into a one-click task

Skip the headaches of juggling multiple IR56 obligations. Sleek’s local accounting experts prepare, review, and e-file the required employer returns on your behalf, sending proactive reminders before any deadline hits. You get transparent pricing, real-time status tracking, and human support whenever questions pop up. Discover how Sleek’s Accounting Services can help keep your business penalty-free so you can focus on hiring and growth.

Sleek is here to help with IR56 Compliance

FAQs about IR56 forms

Who needs to file an IR56 form?

Every Hong Kong employer—be it be company, branch, NGO, partnership, or private household—must file an IR56 for each employee or director who earns Hong Kong-sourced income during the year.

How does IR56 relate to salary tax in Hong Kong?

IR56 forms give the Inland Revenue Department a line-by-line record of each worker’s pay and benefits; IRD uses that data to issue the employee’s annual salary tax assessment.

Do expatriate employees require a separate IR56 form?

No special “expat” version exists. Use the same IR56 series; if the employee is leaving Hong Kong, switch to the IR56G departure form instead of the routine IR56B.

Can individuals submit IR56 forms, or only companies?

Only employers file IR56s. Employees never do. The “employer” can be a corporation, partnership, or even a private resident hiring a domestic helper.

How long should employers keep IR56 records?

Keep all IR56 forms and supporting payroll records for at least 7 years (Inland Revenue Ordinance s.51C).

Is IR56 electronic filing mandatory in 2025?

Yes, if you employ 20 or more people for the 2024/25 year of assessment (filing due April 2025). Smaller employers may still file on paper, but IRD strongly encourages e-filing.

IR56 vs. IRD Employer’s Return—what’s the difference?

The BIR56A Employer’s Return is a one-page payroll summary. The IR56 forms (B, E, F, G, M) are the detailed, employee-specific schedules you attach to that summary.

incorporation, accounting, tax

services, and compliance.

450,000

businesses worldwide.

from 4,100+ reviews.

satisfaction rate from

16,000 surveyed clients.

450,000

businesses worldwide.

from 4,100+ reviews.

satisfaction rate from

16,000 surveyed clients.