With 12 years of industry experience, including a tenure at a Big 4 firm, Yuk Ming is a seasoned professional specializing in accounting, audit, tax, and project management. A member of both HKICPA and ICAEW, he brings a wealth of expertise to Sleek, particularly in advising and supporting SMEs.

Outside work, Yuk Ming enjoys staying active through tennis and badminton. He also likes watching movies and playing video games in his free time.

97% customer satisfaction from 16,000+ survey responses.

In this article

Share this post

Facebook

LinkedIn

WhatsApp

Copy to clipboard

Key takeaways

Hong Kong has no withholding tax on dividends or interest. That’s the biggest misconception about the HK tax system.

Withholding tax applies mainly to royalties paid to non-residents for the use of intellectual property in Hong Kong, and to fees paid to non-resident entertainers and sportspersons.

The general royalty rate to an unrelated non-resident company is 4.95% (or 2.475% on the first HK$6.67 million of gross royalties under the two-tiered regime), because only 30% of the royalty is deemed assessable.

Where the royalty goes to an associate and the IP was once owned by a Hong Kong business, the deemed portion jumps to 100%, so the effective rate is 8.25% / 16.5%.

The Hong Kong payer withholds and remits the tax to the Inland Revenue Department (IRD). A double taxation agreement (DTA) can reduce the rate.

Dividends and interest: no withholding tax in Hong Kong.

Royalties to an unrelated non-resident company: 4.95% (or 2.475% on the first HK$6.67 million of gross royalties under two-tiered rates).

Royalties to an associate (IP once owned by a HK business): 8.25% / 16.5%.

Non-resident entertainer / sportsperson fees: 11% effective for companies (2/3 of gross deemed assessable × 16.5%); 10% for individuals (× 15%).

Who withholds: the Hong Kong payer deducts and remits to the IRD; a DTA can lower the rate.

If you’re paying royalties out of Hong Kong for a trademark, patent or software licence, withholding tax in Hong Kong is the slice you may have to hold back for the IRD rather than pay to the overseas payee. The good news for most founders: Hong Kong’s regime is far narrower than the US or Europe. It doesn’t touch dividends or interest at all.

In this guide, you’ll learn:

What withholding tax is and how it works in Hong Kong

What Hong Kong actually withholds on, and what it doesn’t

The royalty withholding rates, including the higher associate rate

Who has to withhold, remit, and file

How a double taxation agreement reduces the rate

What is withholding tax?

Withholding tax is tax collected at source. In practice, the Hong Kong payer deducts part of the payment, holds it back, and pays it to the IRD on the non-resident’s behalf.

In Hong Kong, withholding tax is not a separate tax type. It is a way of collecting Profits Tax from non-residents earning certain Hong Kong-sourced income, mainly royalties and some performance-related payments. Because the overseas recipient may have no local presence here, the law puts the withholding obligation on the payer instead.

What this means in practice:

The payer is on the hook. If you fail to withhold when required, the IRD can recover the tax from you.

The tax is usually not charged on the full royalty amount. For royalties, a deemed portion of the payment, often 30 percent, is treated as taxable profit first.

It only applies to specific payment types. Dividends, interest, and ordinary service fees generally fall outside the regime, which is why many Hong Kong companies never deal with withholding tax at all.

Yes, but only narrowly. Hong Kong withholds tax on royalties paid to non-residents and on fees paid to non-resident entertainers and sportspersons. It doesn’t withhold on dividends, interest, or ordinary service fees. That makes Hong Kong’s regime much lighter than the US, Mainland China, or most European systems, where dividends and interest are routinely taxed at source.

What doesn’t Hong Kong withhold on: dividends, interest, and service fees?

Hong Kong charges no withholding tax on dividends, interest, or most service fees. If you’ve heard that a “30% withholding tax” applies, that’s another country’s rule, not Hong Kong’s.

Dividends: No withholding tax. A Hong Kong company can pay dividends to shareholders anywhere with nothing deducted, and Hong Kong doesn’t tax dividend income in the recipient’s hands either.

Interest: No withholding tax on interest paid to non-residents.

Service fees: Ordinary fees for services are generally not subject to withholding tax. Tax may still arise if the service income is Hong Kong-sourced profit of the non-resident, but that’s assessed as Profits Tax, not collected by withholding at source.

If you’re paying a dividend or loan interest out of Hong Kong, there’s nothing to withhold.

Good to know

The "30% withholding tax" people search for is usually the US statutory rate on certain US-source payments — or a confusion with Hong Kong's 30% deemed assessable portion on royalties. They're not the same thing. In Hong Kong, 30% is the slice of a royalty treated as taxable profit, not the tax rate. The actual royalty rate works out to 4.95% for an unrelated payee, not 30%.

What are the royalty withholding tax rates in Hong Kong?

Royalties paid to a non-resident for the use of intellectual property in Hong Kong are the main payment that triggers withholding tax, and the rate depends on whether the payee is related to the payer. Because only 30% of the royalty is deemed assessable profit in the normal case, the effective rate works out to a fraction of the headline profits tax rate.

Payment type

Deemed assessable portion

Effective withholding rate (2025/26)

Dividends

—

None

Interest

—

None

Royalty to unrelated non-resident company

30%

4.95% (2.475% on first HK$6.67m gross, under two-tiered rates)

Unrelated non-resident company — 4.95%. The general rate is 30% × the 16.5% profits tax rate. Under the two-tiered regime, the first HK$6.67 million of gross royalties is charged at 2.475% (30% × 8.25%), because HK$6.67 million of royalties equals HK$2 million of assessable profit.

Non-resident individual — 4.5%. The unincorporated rates of 7.5% and 15% apply instead of the corporate rates, giving a general effective rate of 4.5% (30% × 15%).

Associate, IP once HK-owned — 8.25% / 16.5%. This is an anti-avoidance rule. If a person carrying on business in Hong Kong has at any time wholly or partly owned the IP, and the non-resident payee is an associate of the payer, the deemed portion rises from 30% to 100%, so the royalty is taxed at the full profits tax rate, not the reduced effective rate.

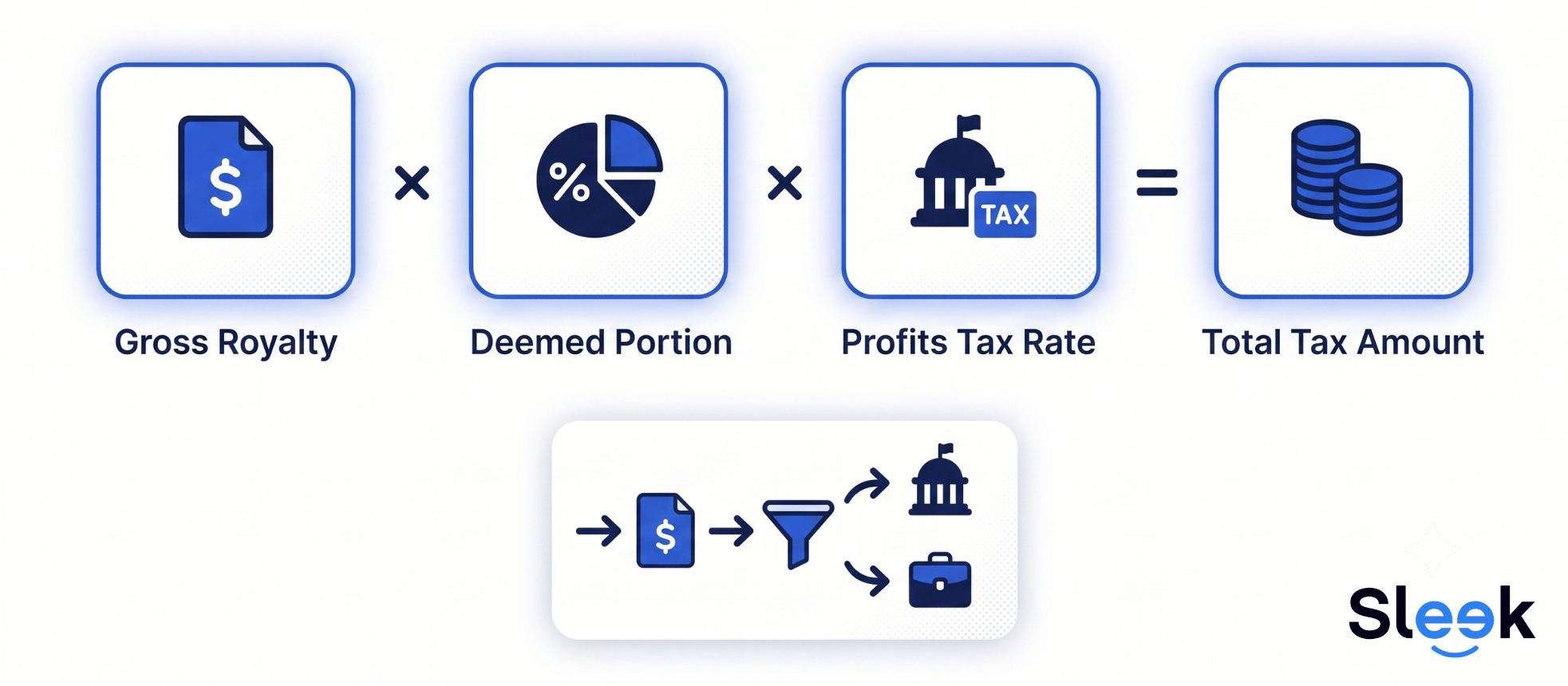

How do you calculate withholding tax on a royalty?

Withholding tax on a royalty is gross royalty × deemed assessable portion × profits tax rate.

Royalty Tax Formula: Understanding the step-by-step calculation

For an unrelated non-resident company in the normal case, that collapses to a single rate on the gross payment:

You pay a HK$100,000 software licence fee to an unrelated non-resident company. You withhold HK$4,950 (100,000 × 4.95%) and remit it to the IRD. The payee receives HK$95,050 net.

The formula shifts in four situations:

Associate + IP once HK-owned: use the 100% deemed portion, not 30%. On HK$100,000, withholding is HK$16,500 (100,000 × 16.5%), not HK$4,950.

Two-tiered rates: the first HK$6.67 million of gross royalties in a year is charged at 2.475%, the balance at 4.95%. On HK$8 million gross: (6,670,000 × 2.475%) + (1,330,000 × 4.95%) = HK$230,618.

Non-resident individual payee: swap in the unincorporated rates (7.5% / 15%) for a general effective rate of 4.5% (30% × 15%).

DTA country: if the treaty caps royalties below the domestic rate, apply the treaty rate on gross once residence is proven.

For entertainers and sportspersons, the deemed portion is 2/3, not 30%, so withholding is gross fee × 2/3 × profits tax rate. For a corporate payee that is gross fee × 11% (2/3 × 16.5%), so a HK$200,000 performance fee means HK$22,000 withheld.

What counts as a royalty?

A royalty is a payment for the right to use intellectual property. In Hong Kong, that covers payments for the use of, or the right to use:

Trademarks and brand names

Patents and designs

Copyrights, including software

Secret processes, formulae, and know-how

Film, tape, or other material used in broadcasting

The common trigger for founders is paying a non-resident group company for a trademark or software licence. If your Hong Kong company licenses IP from an overseas parent or affiliate, those payments are royalties, and the associate rule above is exactly the scenario the IRD watches.

Who has to withhold and remit the tax?

The Hong Kong payer is responsible, not the non-resident who receives the royalty. You deduct the withholding tax from the payment, pay the net amount to the payee, and remit the withheld tax to the IRD.

Getting this wrong is the payer’s problem. If you fail to withhold, the IRD can pursue you for the tax that should have been deducted. Budget the withholding into the contract and confirm the payee’s residency and associate status before you pay.

Important note

You must withhold when you pay or credit the sum, not at year-end. Section 20B(3) of the Inland Revenue Ordinance requires the payer to deduct tax at the time of payment or credit. For royalties, the IRD will issue a Profits Tax Return (Form BIR54) in the non-resident's name under sections 20A/20B; you file that return and pay per the assessment notice. Don't wait for your own company's Profits Tax filing cycle.

How do you file and remit withholding tax?

You withhold at payment, retain the tax, then file the IRD return and pay per the assessment notice. Hong Kong doesn’t use a standalone “withholding tax return.” You’re collecting Profits Tax on behalf of a non-resident, and the payer is chargeable in the non-resident’s name under sections 20A/20B.

Royalties (typical cross-border IP payment):

Confirm the payment is a royalty and work out the rate (associate rule, two-tier, DTA if applicable).

Deduct tax when you pay or credit the non-resident. Pay them the net amount only.

Retain the withheld sum until the IRD issues a demand note or assessment, per DIPN 17.

File Form BIR54 (Profits Tax Return in respect of non-resident persons) when the IRD issues it. GovHK specifies filing within 1 month from the date of issue (the exact due date is on page 1 of the return).

Pay the tax on or before the date shown on the assessment notice. Late payment attracts surcharge and interest.

Non-resident entertainers and sportspersons:

Withhold at the agreed rate (typically 11% or 10% of gross, per the calculation above).

File Form IR623 before the performance or appearance.

Pay once the IRD issues its assessment.

Your own company’s Profits Tax Return (Form BIR51 or BIR52) is a separate filing. That covers your Hong Kong entity’s profits; it doesn’t replace BIR54 for amounts withheld on non-resident royalties.

How does a double taxation agreement reduce the rate?

A double taxation agreement (DTA) between Hong Kong and the payee’s home country can cap the royalty withholding rate below the domestic figure. Treaty royalty limits are often lower than the standard rate, and claiming the treaty rate usually requires the payee to establish treaty residence — typically with a Certificate of Resident Status.

This page covers what Hong Kong withholds; the treaty mechanics, the Certificate of Resident Status, and the foreign tax credit sit in our guide on how DTAs reduce withholding tax. If the payee is in a treaty country, check that guide before applying the domestic rate. The treaty rate may be lower.

When don’t you need to worry about withholding tax?

You’re unlikely to need withholding tax if:

You’re paying dividends or interest to shareholders or lenders — Hong Kong doesn’t withhold on either.

You’re paying ordinary service fees to a non-resident contractor with no IP licence element.

Your payment is for goods, not the use of intellectual property in Hong Kong.

The recipient is a Hong Kong tax resident — withholding targets non-residents without a local filing presence.

If none of those apply and you’re licensing IP from an overseas entity, assume withholding applies until you’ve confirmed otherwise.

When does withholding tax definitely apply?

Withholding tax is in scope if:

You’re paying a non-resident for the use of a trademark, patent, copyright, software licence, or know-how in Hong Kong.

The payee is an associate (often a group company) and the IP was previously owned by your Hong Kong business. The 100% deemed rate applies.

You’re engaging a non-resident entertainer or sportsperson for a Hong Kong performance.

Your contract credits royalties to the payee’s account. Crediting triggers withholding, not just cash payment.

If two or more apply, use the highest applicable rate and document the payee’s residency before you pay.

How Sleek handles your withholding tax

Sleek’s accounting and tax filing team manages withholding tax on cross-border royalty payments: the calculation, the deduction, and the filing. That wat you’re not discovering a payer liability at year-end.

With Sleek, you can:

Get the rate right the first time: We confirm whether a payment is a royalty, whether the associate rule applies, and the correct effective rate, so you withhold 4.95% or 16.5% as the facts require, not a guessed figure.

Withhold and remit on schedule: We calculate the amount, prepare the deduction, and file with the IRD, keeping the payer obligation off your desk.

Apply treaty relief where it exists: Where the payee sits in a DTA country, we check the treaty rate and residence evidence before you pay, coordinating with our audit and tax services for group IP arrangements.

Structure IP holdings cleanly: For founders centralising IP, we advise alongside our Hong Kong holding company and IP guidance so royalty flows and the associate rule are planned — not accidental.

Paying royalties or performance fees to non-residents?

Talk to Sleek about your cross-border payments and withholding obligations. Accounting plans from HK$3,500.

Is withholding tax the same as Profits Tax in Hong Kong?

Yes, in substance. Hong Kong doesn’t have a separate withholding tax regime. It’s Profits Tax collected at source from non-residents on Hong Kong-sourced royalties and performance fees. The payer withholds an amount based on deemed assessable profits (30% or 100% for royalties; two-thirds for entertainers) and the applicable Profits Tax rate.

When exactly do I have to withhold: at payment or year-end?

At payment or credit, whichever comes first. Section 20B(3) requires the Hong Kong payer to deduct tax when the sum is paid or credited to the non-resident. You don’t wait until your own Profits Tax Return is due. Ring-fence the withheld amount and file the IRD return (typically Form BIR54 for royalties) when issued.

What if my group company owns the IP overseas: does the associate rule still apply?

It can. If the IP was at any time wholly or partly owned by a person carrying on business in Hong Kong, and the non-resident recipient is an associate of the payer, the deemed assessable portion rises to 100%, pushing the effective rate to 8.25% / 16.5%. This is the classic group-licence scenario. Document the IP ownership history before you structure royalty flows.

Can the overseas payee claim a refund if too much was withheld?

The non-resident can file a Hong Kong Profits Tax Return and claim treaty relief or a lower rate if they’re entitled to one, for example under a DTA with a reduced royalty cap. The payer’s job is to withhold at the correct rate upfront; any refund or adjustment happens on the non-resident’s assessment, not by skipping withholding.

Can Sleek calculate and file withholding tax on our royalty payments?

Yes. Sleek’s tax team handles the rate calculation, the deduction at payment, and IRD filing for cross-border royalty and performance-fee payments. Talk to our tax team if you’re paying royalties to a non-resident group company or licensing IP from overseas.