- A deductible expense is a cost you incurred to earn your business profits. Subtract it from your revenue, and you pay Profits Tax only on what’s left.

- Hong Kong’s two-tier Profits Tax rate means your first HK$2 million in assessable profits is taxed at 8.25% (corporations) or 7.5% (unincorporated businesses). Everything above that is taxed at 16.5% or 15%.

- The IRD requires you to keep records for at least seven years. No receipt, no deduction — it’s that simple.

- Some expenses get enhanced deductions: qualifying R&D costs are deductible at 300% for the first HK$2 million, and computer hardware and software get a 100% write-off in the year of purchase.

Every dollar you can legitimately deduct from your revenue is a dollar that isn’t taxed. For a company earning HK$3 million in profits, the difference between claiming HK$400,000 in deductible expenses and missing HK$100,000 of them is roughly HK$16,500 in extra tax paid — money that could have stayed in your business.

This guide covers what you can deduct, what you can’t, what records the Inland Revenue Department (IRD) expects, and the mistakes that get claims rejected.

How do Profits Tax deductions work?

Under the Inland Revenue Ordinance (Cap. 112), a business expense is deductible if it was incurred “in the production of” your assessable profits. The IRD’s test is straightforward: was this a day-to-day cost that was necessary to generate your company’s income during that assessment year?

If yes, you deduct it from your gross revenue. The result is your assessable profit, and that’s what you pay tax on.

If your company earns HK$2 million in revenue and has HK$1.2 million in deductible expenses, your assessable profit is HK$800,000. At the two-tier rate, your entire tax bill falls within the 8.25% band, so you'd owe HK$66,000.

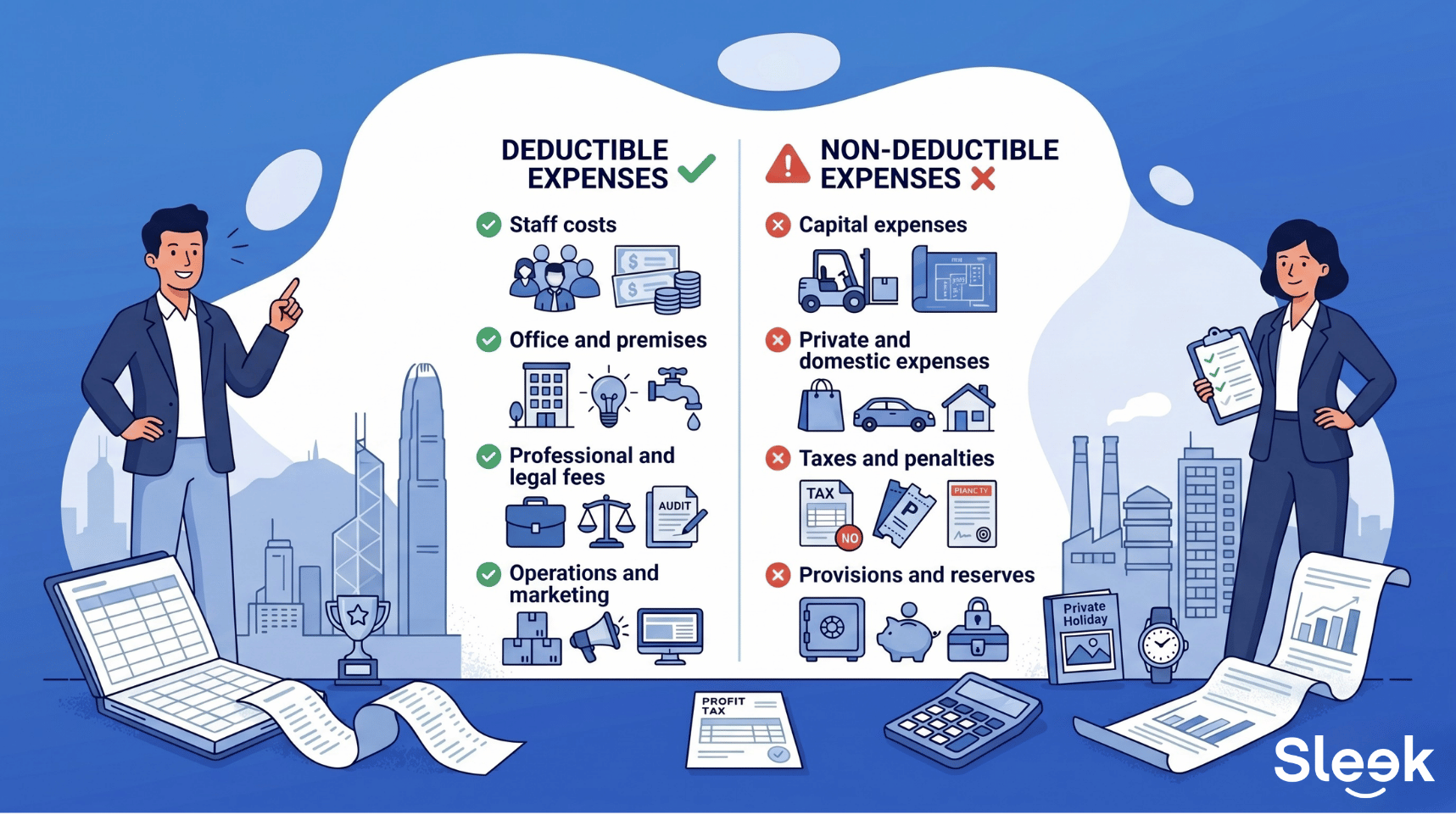

Which business expenses are deductible?

Staff costs

- Salaries, wages, commissions, bonuses, and staff allowances

- Employer’s MPF contributions (mandatory and voluntary, up to the deductible limit)

- Severance payments and long service payments required by law

- Staff training and development costs

- Recruitment agency fees

Office and premises

- Rent for your office, shop, or warehouse

- Utilities (electricity, water, business internet)

- Building management fees and government rates

- Repairs and maintenance of premises and equipment — but not improvements (improvements are capital)

Professional and legal fees

- Accounting, audit, and bookkeeping fees

- Legal fees for business operations (debt collection, contract disputes)

- Consultancy fees directly related to earning profits

- Bank charges and transaction fees

- Interest on business loans used to produce profits

Operations and marketing

- Cost of trading stock, raw materials, and inventory

- Advertising, digital marketing, and PR expenses

- Business entertainment expenses (meals with clients, events)

- Business travel (flights, hotels, local transport for client visits)

- Software subscriptions and SaaS tools used in operations

Enhanced and special deductions

These categories get better-than-standard treatment from the IRD:

Expense type | Deduction rate | Notes |

|---|---|---|

Qualifying R&D expenditure (first HK$2M) | 300% | Must be carried out in Hong Kong; Section 16B of Cap. 112 |

Qualifying R&D expenditure (above HK$2M) | 200% | Same conditions apply |

Computer hardware and software | 100% in year of purchase | Full write-off, no need to depreciate |

Environmentally friendly machinery/equipment | 100% in year of purchase | Must meet prescribed criteria |

Building refurbishment | 20% per year for five years | Total 100% deduction spread over five years |

Approved charitable donations | Up to 35% of assessable profits | Must be to an IRD-approved organisation |

Depreciation allowances (capital allowances)

You can’t deduct the full cost of a major asset in one year (that’s a capital expense). Instead, you claim depreciation allowances:

Asset type | Initial allowance | Annual allowance |

|---|---|---|

Plant and machinery | 60% | 10%, 20%, or 30% (depending on asset category) |

Industrial buildings | 20% | 4% |

Commercial buildings | — | 4% |

The initial allowance applies in the year you buy the asset. The annual allowance applies to the remaining value each year after that.

Which business expenses are non-deductible?

Capital expenses

- Purchase cost of fixed assets (property, vehicles, major equipment) — claim depreciation allowances instead

- Any expense that improves an asset beyond its original condition (as opposed to restoring it)

- Costs incurred before your business started trading (pre-commencement expenses)

Private and domestic expenses

- Any cost not directly related to producing your business profits

- Owner’s drawings or salary if you’re a sole proprietor or partner

- Travel between your home and your regular workplace (commuting)

- Personal medical bills, life insurance, or household costs

Taxes and penalties

- Profits Tax itself is not deductible

- Fines or penalties for breaking any law (parking tickets, regulatory penalties, late filing surcharges)

Provisions and reserves

- General provisions for doubtful debts (you can only deduct a bad debt once it’s formally written off and was previously included as income)

- Contributions to retirement schemes not approved by the IRD

- Capital losses

Quick summary of deductible and non-deductible business expenses

What records does the IRD expect?

The IRD’s position is simple: if you claim it, you need to prove it. Your company must keep business records for at least seven years, even after the business closes. If the IRD selects your return for review, they’ll ask for these:

1. Invoices and receipts

The primary proof for any expense. Each one should show the vendor name, date, description, and amount.

2. Bank and credit card statements

These confirm that money actually left your account for the expenses you’ve claimed.

3. Contracts and agreements

Tenancy agreements, employment contracts, loan agreements — anything that justifies a major or recurring cost.

4. Payroll records

Detailed records of every payment to staff: salaries, bonuses, commissions, and MPF contribution statements.

5. Expense reimbursement forms

For staff travel or client entertainment, you need a record of the date, amount, business purpose, and who was involved — attached to the receipt.

6. General ledger and books of account

Your complete accounting records, summarising every transaction your business made during the year.

Sample Chart of Accounts for tracking deductible expenses

A well-organised Chart of Accounts (COA) makes Profits Tax filing simpler because it separates deductible and non-deductible items from the start. Here’s a sample for a small service or trading business in Hong Kong.

5000 — Cost of Goods Sold (COGS) (fully deductible if you sell physical products)

- 5100: Purchases — Raw Materials

- 5200: Purchases — Finished Goods for Resale

- 5300: Freight and Shipping Inwards

6000 — Operating Expenses (day-to-day costs; most are fully or partially deductible)

- 6100 — Staff Costs: 6110 Salaries & Wages, 6120 Commissions & Bonuses, 6130 MPF Contributions (Employer), 6140 Staff Training, 6150 Staff Welfare, 6160 Severance & Long Service Payments

- 6200 — Office & Premises: 6210 Rent, 6215 Rent — Home Office (apportioned; track separately), 6220 Government Rates, 6230 Management Fees, 6240 Utilities, 6250 Internet & Telephone

- 6300 — Professional & Legal Fees: 6310 Accounting & Audit, 6320 Legal Fees (business operations), 6330 Consultancy Fees

- 6400 — Sales & Marketing: 6410 Advertising & Promotion, 6420 Business Entertainment, 6430 Website Hosting & Software Subscriptions, 6440 Marketing Services

- 6500 — Travel: 6510 Airfare, 6520 Accommodation, 6530 Local Transport (business, not commuting)

- 6800 — General Business: 6810 Bank Charges, 6820 Business Insurance, 6830 Office Supplies, 6840 Repairs & Maintenance (not improvements), 6850 Approved Charitable Donations

6900 — Non-Deductible Expenses (separate category makes tax calculation easier)

- 6910: Fines & Penalties

- 6920: Legal Fees — Capital Nature (company setup, asset purchase)

- 6930: Profits Tax Paid

Capital assets (computers, vehicles, equipment) go into Asset accounts on your balance sheet (1700 range), not expense accounts. You claim depreciation allowances on those separately.

Five common reasons the IRD rejects deduction claims

1. No receipt or insufficient evidence

The most common rejection. If you can’t produce a valid invoice, receipt, or bank statement when the IRD asks, the deduction is disallowed. Digital records are acceptable, but they must be complete and retrievable.

2. The expense wasn’t for business purposes

Any cost the IRD determines was private or domestic gets rejected. “Wholly and exclusively” is the test — the sole reason for the expense must have been to produce business profits. Mixed-use expenses (like a phone used for both business and personal) must be apportioned.

3. Capital expense claimed as a revenue expense

You can’t deduct the full cost of a vehicle, major renovation, or significant equipment purchase in one year. These are capital expenses — you claim depreciation allowances on them over their useful life instead.

4. The business purpose isn’t documented

A dinner receipt on its own isn’t enough. If you can’t explain who you met, what business topic was discussed, and how the meeting relates to earning your profits, the IRD may reject it as a private expense. Keep a note with every entertainment receipt.

5. Pre-commencement expenses

Costs incurred before your business officially started trading are capital in nature. This includes company formation fees and setup costs before you began generating revenue. These are not deductible against your profits.

Get your tax deductions right with Sleek

Getting your deductions wrong costs you twice: once when you overpay tax by missing a legitimate claim, and again when the IRD rejects an expense you should not have included. Both problems come down to the same thing: poor records.

Sleek takes care of that from day one with:

- Accurate bookkeeping from the start: Sleek’s accounting and bookkeeping service categorises every expense correctly against a Hong Kong-specific chart of accounts, so nothing is missed and nothing is misclassified.

- Audit-ready records at tax time: When your Profits Tax Return is due, your books are already in order and every deduction you are entitled to is accounted for.

- No surprises at year end: Audit and tax filing packages are transparent and all-inclusive. You know exactly what you are paying before we start.

Sleek handles your bookkeeping, tax computation, and Profits Tax filing, so nothing gets missed and nothing gets rejected.

450,000

businesses worldwide.

from 4,100+ reviews.

satisfaction rate from

16,000 surveyed clients.

FAQs about deductible and non-deductible business expenses in Hong Kong

View more