Corporate taxable income, also known as profits tax in Hong Kong, is figured out based on a company’s assessable profits. These profits are determined by adjusting the company’s net profit and loss accounts for the taxable period.

This guide provides a step by step guide on how to calculate Hong Kong company tax.

Need help with corporate tax calculations?

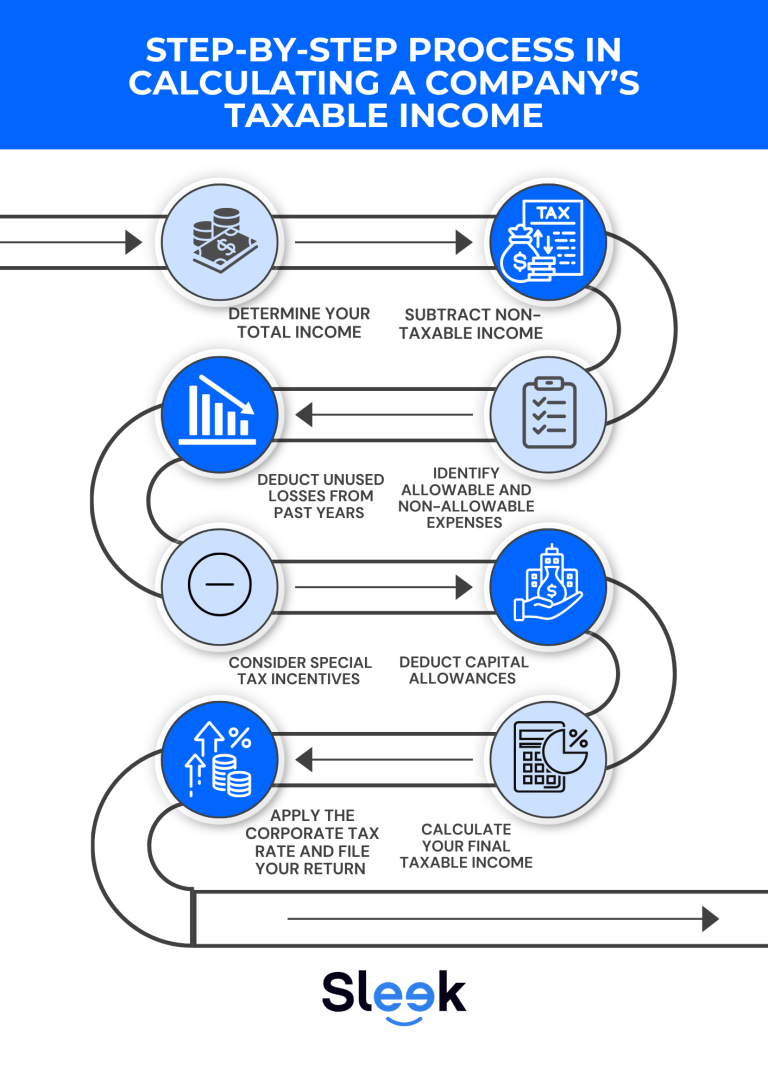

Step-by-step process to calculate corporate income tax in Hong Kong

Here is a step-by-step guide to calculating your business income tax in Hong Kong.

Step 1: Determine your total income

First, identify all the money your business has earned. This includes revenue from your main business activities, like selling goods or providing services, as well as other income like rent you received from property.

Step 2: Subtract non-taxable income

Next, you need to remove any income that is not taxed in Hong Kong. You should subtract:

- Profits from outside Hong Kong: This is also known as offshore tax exemption. It means you only pay tax on profits made in Hong Kong.

- Capital Gains: Money you make from selling capital assets (like an office building or equipment) is not taxed.

- Certain Dividends: Dividends you receive from another company that has already paid Hong Kong company profit tax are exempt.

- Some Interest Income: Interest you earn from bank deposits is usually not taxed, unless receiving interest is a core part of your business.

Step 3: Identify allowable and non-allowable expenses

Look at all the expenses you subtracted to find your net profit. You need to separate them into two groups: expenses that are allowed for tax deductions and those that are not.

- Allowable expenses: These are costs directly related to running your business, like employee salaries, office rent, utilities, and marketing.

- Non-allowable expenses: These include costs like personal expenses, fines, penalties, and most donations. You will need to add these back to your profit in Step 7.

Step 4: Deduct unused losses from past years

If your business had losses in previous years, you can subtract those “unabsorbed” losses from your current year’s profits. This helps lower your corporate income tax for the year.

Step 5: Deduct capital allowances

Instead of deducting the accounting depreciation of your assets, you deduct capital allowances. These are the tax deductions you can claim for the cost and wear-and-tear of business assets like machinery, equipment, and computers.

Step 6: Consider special tax incentives

Check if your company can use any Hong Kong business tax incentives offered by the government. For example, you can get extra deductions for money you spend on qualifying research and development (R&D) activities.

Step 7: Calculate your final taxable income

This is the most important step in calculating Hong Kong corporation tax, where you put everything together. Follow this formula to find your final taxable income:

- Start with your company’s net profit for the year (from your profit and loss account).

- Add (+) any expenses that are not allowed for tax purposes (e.g., fines, personal expenses).

- Subtract (-) any income that is not taxable (e.g., capital gains, profits from outside Hong Kong).

- Subtract (-) capital allowances for your business assets.

- Subtract (-) any unabsorbed losses from previous years.

The final number is your Taxable Income.

Step 8: Apply the corporate tax rate and file your return

Once you know your taxable income, you can calculate your tax. Apply the two-tiered tax rate: 8.25% on the first HK$2 million of profit and 16.5% on the rest. Finally, complete your Profits Tax Return and file it with the Inland Revenue Department (IRD) by the deadline.

Taxable income calculation

Let’s use the example of a consulting firm in Hong Kong. Their financial statements show a Net Income of HK$1,500,000 for the year.

To determine the firm’s taxable income, we must adjust this figure based on the tax rules. Below is a summary of the calculation.

Description | Amount (HK$) |

Net Income as per Accounts | 1,500,000 |

Add back items not deductible for tax: | |

Accounting Depreciation | 200,000 |

Donations to a non-approved charity | 25,000 |

Subtract items not taxable or specially deductible: | |

Offshore income from a UK project | (150,000) |

Capital Allowances (tax-deductible depreciation) | (250,000) |

Unused business losses from the prior year | (300,000) |

Final Taxable Income | 1,025,000 |

Final tax calculation

The business’s taxable income is HK$1,025,000. Since this is below the HK$2 million threshold, it is taxed at the lower rate of 8.25%.

- Final Tax Payable = HK$1,025,000×8.25%=HK$84,562.50

What is included in a Hong Kong business’s net income?

A Hong Kong business’s net income, often called net profit or net earnings, represents the amount of money remaining from its revenues after subtracting all expenses, taxes, and costs.

It is a crucial metric that gives insight into the actual profitability of a business over a specific period. For a Hong Kong business, net income includes several components:

- All sources of revenue:

- Trading profits (core business activities)

- Investment income (interest, dividends, certain royalty income)

- Rental income

- Capital gains (even if some aren’t subject to tax)

- Income from sources outside of Hong Kong

- Deductible expenses: This is a broad category but typically includes)

- Cost of goods sold

- Operational expenses (e.g., rent, salaries, utilities)

- Depreciation of assets

- Interest expenses on business loans

- Bad debts (subject to conditions)

- Tax-deductible charitable donations

How net income is calculated

Net Income = Total Revenues−COGS−Operating Expenses−Depreciation and Amortization−Interest Expenses−Taxes+Other Incomes−Other Expenses

Hong Kong Taxation: A Complete Guide to Profits & Salaries Tax

What is the difference between net income and taxable income?

Net income represents the business’s overall profit after subtracting deductible expenses.

Taxable income is a narrower figure calculated after making additional adjustments based on specific Hong Kong tax regulations.

Here is a table summarizing the key differences between Net Income and Taxable Income in the context of Hong Kong Corporate Tax:

Category | Net Income | Taxable Income |

Definition | The total profit your business makes after subtracting all of its expenses. This is an accounting figure. | The specific portion of your profit that you must pay taxes on, calculated according to government tax laws. |

Purpose | To show how profitable your company is to shareholders, investors, and managers. | To calculate the exact amount of profits tax your company owes to the Inland Revenue Department (IRD). |

How it’s calculated | Based on standard accounting principles. You can find this number on your company’s audited financial statements. | Starts with your net income, which is then adjusted based on the rules in the Inland Revenue Ordinance. |

What it Includes | You subtract all operating expenses from your total revenue. | You adjust your net income by adding back expenses that aren’t allowed for tax purposes and subtracting income that isn’t taxable. |

Governed by | Accounting standards and financial reporting requirements. | Tax laws and regulations set by the Inland Revenue Department (IRD). |

Where you use it | In your company’s financial reports, like the Income Statement, for investors and internal use. | On your official Profits Tax Return form that you file with the government. |

Why is understanding net income important?

Net income gives stakeholders a clear view of a company’s profitability and financial health after all financial obligations have been met, including tax liabilities.

It’s a key indicator used in financial analysis, valuation, and assessing the efficiency and profitability of a business’s operations.

Pro tip: One CoR usually covers the claim year plus the next two calendar years, so you won’t need to reapply every year.

Stay compliant and stress-free with Sleek

Calculating your company’s taxable income can be complex. You don’t have to manage it all on your own. Let the experts at Sleek handle your accounting and taxes so you can focus on what you do best—growing your business. We help you stay compliant and give you complete peace of mind.

Our team ensures your finances are accurate and ready for filing. Learn more about how our audit services can help you succeed.

Sleek is here to help in calculating your company's taxable income

FAQs about how to calculate company tax in Hong Kong

Are capital gains subject to taxation in Hong Kong?

No, capital gains are not subject to taxation in Hong Kong. However, profits derived from trading in stocks or properties may be subject to profits tax if they are considered part of a business operation.

Who has to pay corporate tax in Hong Kong?

All corporations, partnerships, trustees, and organizations conducting trade, profession, or business in Hong Kong are subject to Profits Tax on profits arising in or derived from Hong Kong. Offshore profits are generally not taxable unless they are deemed to have a Hong Kong source.

What are the current profits-tax rates for SMEs vs. large companies in Hong Kong?

Hong Kong follows a two-tiered Profits Tax system:

- For corporations:

- 8.25% on the first HK$2 million of assessable profits.

- 16.5% on any remaining profits.

- For unincorporated businesses (e.g., partnerships or sole proprietorships):

- 7.5% on the first HK$2 million.

- 15% on the remaining profits.

Only one entity among connected entities can benefit from the reduced first-tier rate.

Does Hong Kong offer any tax incentives for startups or tech firms?

Yes, Hong Kong provides several incentives:

- The two-tier profits tax rates favor startups.

- Super deduction of 300% for the first HK$2 million and 200% thereafter for qualifying R&D expenses.

- Various government funding schemes such as the Innovation and Technology Fund (ITF) and Cyberport Creative Micro Fund, which, while not direct tax incentives, support innovation with financial assistance.

incorporation, accounting, tax

services, and compliance.

450,000

businesses worldwide.

from 4,100+ reviews.

satisfaction rate from

16,000 surveyed clients.

450,000

businesses worldwide.

from 4,100+ reviews.

satisfaction rate from

16,000 surveyed clients.