What is negative gearing?

Gearing in property investment simply means you borrow money to purchase an asset. Negative gearing happens when your investment property costs more to own than the property income it generates. The rental income you receive is not enough to cover all the rental expenses, such as loan interest, council rates, and maintenance costs.

This situation results in a net rental loss for the financial year. The reason an investor might choose a negatively geared property lies within the Australian tax system. You are allowed to offset losses against your other income.

Key points:

- Investors can often claim this net rental loss as a tax deduction against their other taxable income, like a salary.

- This deduction lowers your total taxable income, which can reduce the amount of tax you pay.

- It’s a strategy focused on future capital growth, hoping the property’s value increases over time to provide a substantial capital gain upon sale.

How to calculate negative gearing in 3 steps

Figuring out if a property is negatively geared is straightforward. You need to use a simple gearing calculation. It subtracts your total expenses from your total property income for the year.

The basic formula for calculating negative gearing is:

Total Rental Income – Total Deductible Expenses = Net Rental Profit or Loss.

If you get a negative number, the property is negatively geared.

Step 1: Determine your assessable rental income

First, you must calculate all the income the geared property generates. The main component is the gross annual rental income paid by your tenants. This is the full amount before any property management fees are taken out.

Other income sources could also apply to the rental income sum. This might include payments from tenants for ending a lease early or insurance payouts for lost rent. You must add all these amounts together to get your total annual rental for the full year.

Step 2: List all your deductible expenses

Next, you must add up every tax-deductible expense related to the rental property. This list of property expenses can be long and includes many costs associated with holding the asset. These are costs you paid for during the financial year the property was available for rent.

Being thorough here is important, as missing expenses will lead to an incorrect negative gearing calculation. You can use a negative gearing calculator or a gearing calculator tool to help track these figures. This ensures you account for all potential claims.

Step 3: See if you have a loss

Finally, subtract your total expenses from your total income. This reveals the property’s financial performance for the year. A negative result confirms a net rental loss, which means the asset is a negatively geared property.

Let’s look at a practical example. This makes the concept much easier to understand.

| Item | Amount (per year) |

|---|---|

| Gross rental income | $28,000 |

| Total deductible expenses: | |

| Investment loan interest payments | $25,000 |

| Council rates | $2,000 |

| Water rates | $1,000 |

| Body corporate fees | $3,000 |

| Insurance premiums | $1,500 |

| Repairs and maintenance | $2,500 |

| Property management fees | $2,240 |

| Depreciation | $4,000 |

| Total Expenses | $41,240 |

| Net Rental Profit/(Loss) | Gross rental income- total expenses $28,000-$41,240 -$13,240 |

In this scenario, the annual loss is $13,240. This property is clearly negatively geared. This is the figure you can potentially use to offset your other income.

Tracking all of this information correctly is critical. Getting these figures right will have a direct impact on your tax return. If you need help with your specific situation, you can get a fixed-price accounting quote for professional support.

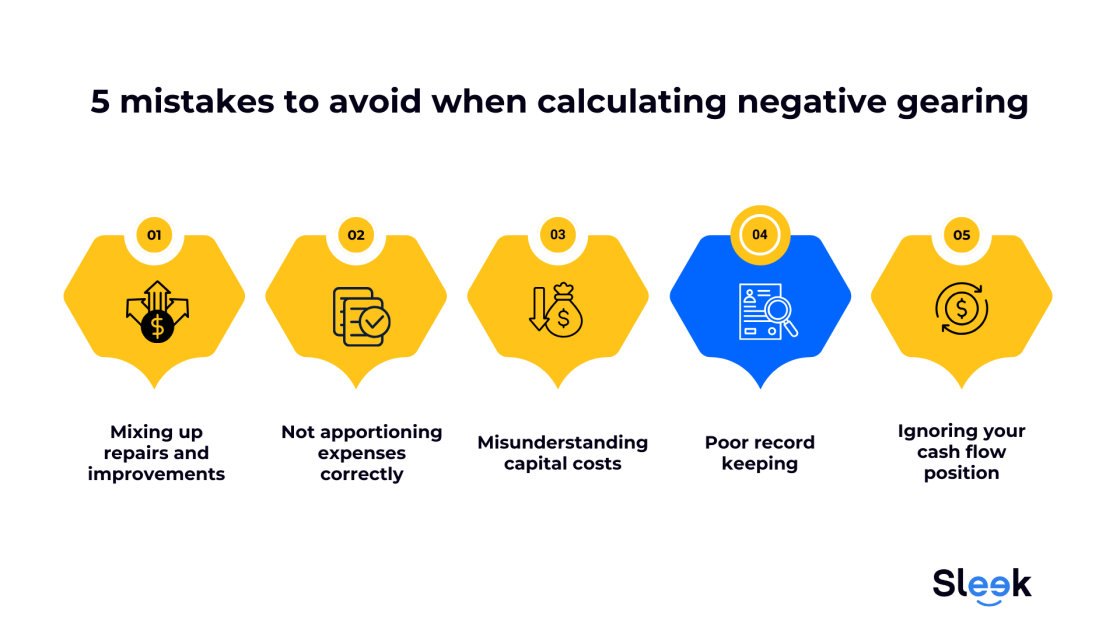

5 mistakes to avoid when calculating negative gearing

When you’re working through how to calculate negative gearing, mistakes can be costly. They can lead to issues with the ATO or missed financial opportunities. Here are some frequent errors to watch out for.

1. Mixing up repairs and improvements

A big mistake is incorrectly classifying your spending. The ATO sees repairs and improvements very differently. A repair restores something to its original condition.

An improvement makes something better than it was before.

For example,

- Replacing a broken fence panel is a repair and is immediately deductible.

- Replacing the entire old fence with a new, more modern one is a capital improvement, which must be depreciated over many years.

2. Not apportioning expenses correctly

You can only claim expenses for the portion of the property and time it was used to earn income. If you live in a duplex and rent out the other half, you can only claim 50% of shared costs. The same applies if you use your holiday home for personal getaways.

- You must accurately divide costs like loan interest and council rates.

- Strict rules also apply to travel expenses; you generally cannot claim travel to inspect a residential rental property unless you are in the business of property investing.

- Claiming private or personal expenses, such as interest on your family home loan or car loans for personal use, is not permitted.

You must separate these costs from your genuine investment expenses.

3. Misunderstanding capital costs

Many initial costs of buying a property are not immediately deductible against your rental income. Expenses like stamp duty, conveyancing, and legal fees associated with the purchase are capital costs. These items form part of the property’s cost base.

- The cost base is used to calculate your capital gains tax when you eventually sell the property.

- Confusing these with day-to-day rental expenses is a common error.

- This can lead to incorrectly claiming a tax deduction now instead of reducing your future capital gains.

4. Poor record keeping

Solid record keeping is not optional. The ATO requires you to keep detailed records for all income and expenses for at least five years. This includes receipts, bank statements, and agent summaries.

Without proper proof, your claims can be denied if you are audited. Using spreadsheets or accounting software can make this process much easier. It prevents stress at tax time and protects you if the ATO has questions about the claims you’re making.

5. Ignoring your cash flow position

Focusing only on the tax benefits is a trap. You must have enough money to cover the property’s losses each month. Running out of cash could force you to sell at a bad time, potentially losing money on your investment.

Before you invest, you need a clear budget. Understand how much you’ll need to contribute every week or month. This helps make sure the investment is sustainable for the long term.

Conclusion

Negative gearing is a well-known investment approach in Australia. It allows a property investor to offset a property’s net loss against their other taxable income. The main goal is to benefit from tax reductions now while aiming for capital gain in the future.

Now you know how to calculate negative gearing by subtracting your total expenses from your annual rental income. The success of this strategy is not guaranteed. It depends on strong property market growth to offset the short-term cash flow losses and generate a profit.

Understanding the formula, claimable expenses, and maintaining perfect records are essential parts of the process. Properly managing your approach to how to calculate negative gearing can make a real difference in your property investment journey.

How Sleek can help you maximize your negative gearing benefits

Negative gearing can be a powerful strategy but only if your numbers are accurate and your tax claims are watertight. That’s where Sleek’s property accountants comes in.

- Precise record-keeping: Track every deductible expense so you never miss a claim.

- ATO-ready reporting: Get compliant, accurate statements for tax time without the stress.

- Cash flow planning: Forecast and manage shortfalls so your investment remains sustainable.

- Expert property tax advice: Sleek’s dedicated accountants specialise in local investment property tax rules, ensuring you make the most of available benefits.

Book a free consultation today and let Sleek’s experts turn property losses into strategic tax wins.