Grow your business seamlessly with hassle-free accountant services!

Feeling like your business has outgrown your accountant? Or maybe you’re just not vibing with their style anymore? Have you been thinking of how to switch accountants lately? Switching accountants can seem like a big deal, but it doesn’t have to be a stressful experience. With the right approach, you can make the transition smooth and efficient.

Think of it like changing your mobile phone provider. You wouldn’t stay with a provider that no longer meets your needs, right? Your accountant is a crucial part of your business team, and it’s essential to have one that aligns with your long-term financial goals and provides the support you need to thrive.

This guide walks you through the steps on how to switch accountants, from finding the perfect fit for your business to ensuring a seamless handover of your financial information.

Signs it’s time to switch accountants

Just like any professional relationship, the dynamic between you and your accountant is important. If something doesn’t feel right or you’re not getting what you need, it might be time to consider finding a new accounting partner. Here are a few common reasons why business owners choose to change accountants:

Outgrowing your current accountant

As your business evolves, so do your accounting needs. What worked for you as a startup might not be cut when dealing with increased revenue, more complex tax obligations, or international expansion.

Here are some signs you might have outgrown your current accountant:

- Changes in business structure: Have you transitioned from a sole trader to a company? Or perhaps you’ve added new business partners? These changes often require more specialised accounting expertise.

- Expansion into new markets: Selling goods or services overseas introduces a whole new layer of complexity to your finances, including foreign currency transactions and international tax laws.

- Increased complexity of financial operations: Perhaps you’ve secured a significant investment, acquired another business, or are dealing with more sophisticated financial instruments. These situations demand an accountant with advanced knowledge and experience.

If any of these scenarios resonate with you, it might be time to seek an accountant who can better handle the increasing complexity of your business finances.

Lack of industry expertise

Accountants should provide insight tailored to your business’s specific needs and challenges. A lack of familiarity with your industry could lead to missed opportunities or incorrect advice. If you’re an e-commerce company dealing with sales tax and international shipping or a dentist requiring specialised accounting knowledge, ensure your accountant has relevant experience.

Poor communication or unresponsiveness

Are you constantly chasing your accountant for updates or struggling to get them on the phone? Clear communication and responsiveness are crucial in an accountant-client relationship. Waiting weeks for a reply or feeling ignored is a sign it may be time to move on. If you find yourself seeking more than just basic accounting services, such as tax planning or financial forecasting, it may be time to consider changing accountants.

Technology gap

Cloud accounting software has become a game-changer for businesses. Sage’s 2020 Practice Of Now report found that nearly half of accounting firms experienced significant efficiency boosts after incorporating technology. Your accountant should be leveraging these tools to provide faster, more accurate service and support your evolving digital needs. Ask potential accountants about their familiarity and usage of online accounting software to determine if they align with your expectations.

Lack of proactive advice

Modern accountants go beyond simply crunching numbers—they should actively seek to add value to your business. Are they providing strategic tax planning, advising on cash flow, or helping you anticipate challenges? If your accountant is stuck in a “checkbox accounting” mindset, it might hinder your growth potential. Look for a new accountant who will proactively provide tax and planning advice that can help you save money and reach your financial goals.

Cost Considerations

While cost shouldn’t be the sole deciding factor when choosing an accountant, it’s important to ensure that your fees align with the value you’re receiving. Accountants typically charge in one of three ways:

- Hourly rates: You pay for the actual time spent on your work.

- Fixed fees: You agree on a set price for specific services.

- Value pricing: Fees are based on the value the accountant delivers to your business.

No matter the pricing structure, transparency is key. You should clearly understand what you’re being charged for and how those costs relate to the services provided. Don’t hesitate to ask for a detailed breakdown of fees and compare quotes from different accountants to ensure you get the best value for your money.

Remember, the cheapest option isn’t always the best. When evaluating the overall value proposition, consider the accountant’s experience, expertise, and the level of support they offer.

Sometimes, one of the best ways on how to switch accountants is to invest in a more experienced accountant, which can lead to significant long-term cost savings through proactive advice, tax planning strategies, and improved financial efficiency.

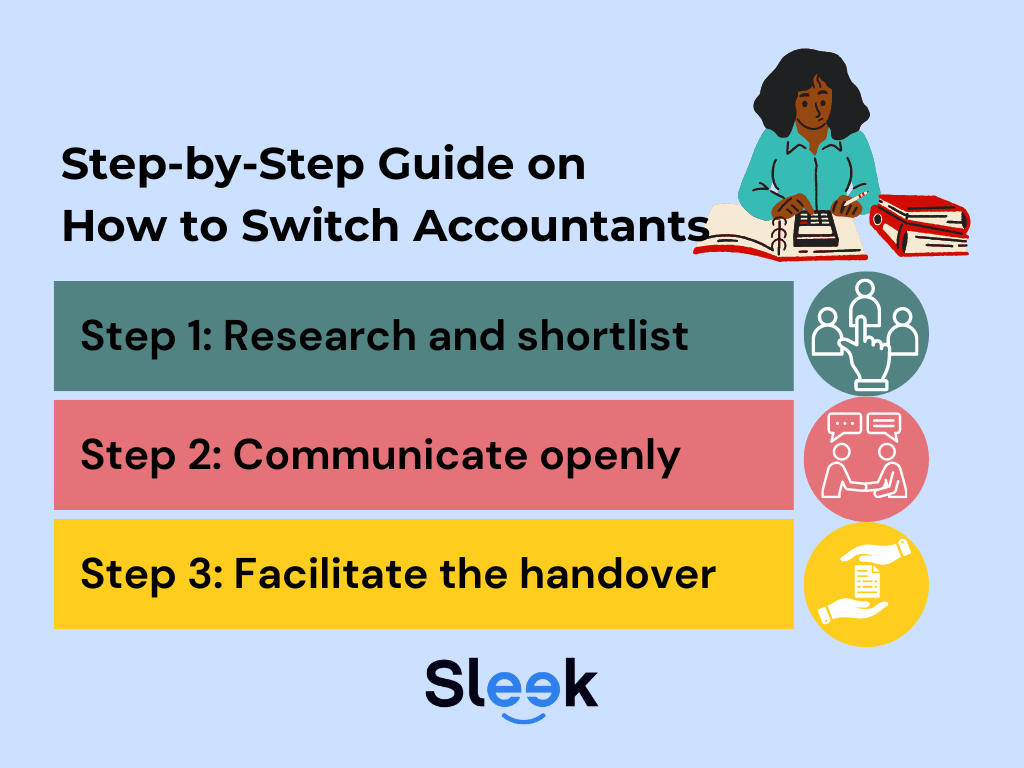

Step-by-step guide on how to switch accountants

The idea of how to switch accountants might seem disruptive, but if you approach it strategically, it can be a surprisingly smooth process. Follow these key steps to change accountants seamlessly:

Step 1: Research and shortlist

Choosing a new accountant is a crucial step. Take your time to find someone who fits your business needs and with whom you feel comfortable sharing your financial information.

Before you start your search, consider what you’re looking for. Do you need an accountant with experience in your specific industry?

Is your business at a stage where you need a larger firm with a broader range of services? Are you looking for basic bookkeeping and tax preparation, or do you need assistance with financial planning and business consulting?

Once you understand your needs well, seek recommendations from other business owners, industry associations, or online directories. Word-of-mouth can be a valuable tool in finding a reputable accountant who understands the challenges and opportunities facing businesses like yours.

When you have a shortlist of potential accountants, schedule interviews to get a feel for their personality, experience, and communication style. Come prepared with questions about their experience working with similar businesses, fees, approach to communication, and availability.

Pay attention to how they answer your questions and whether they seem genuinely interested in your business and its success. Can they explain complex financial concepts in a way you understand? Do they inspire confidence and trust?

When choosing a new accountant, ensure they are registered with a recognised professional body in Australia like Chartered Accountants ANZ. This guarantees they meet the industry’s ethical and professional standards.

Additionally, consider whether the accountant has any specific certifications or affiliations relevant to your business, such as being a registered tax agent or having experience in a particular industry. For instance, if you need property investment advice, ensure they possess the relevant expertise.

Step 2: Communicate openly

Have an honest conversation with your current accountant about your decision. It doesn’t need to be a dramatic confrontation. A simple written notice outlining your intentions, including the effective date of the switch, is sufficient.

Before switching, be sure to discuss any outstanding fees or incomplete work. Settling any financial obligations with your current accountant is important to ensure a smooth transition.

Step 3: Facilitate the handover

This step on how to switch accountants involves the transfer of sensitive financial information, so it’s important to understand how the handover process works and what you can expect from both your old and new accountants.

Professional conduct

Rest assured that the handover of your financial information is governed by strict ethical guidelines set by professional accounting bodies. Your old and new accountants must act with professionalism and integrity throughout the process. This includes maintaining confidentiality, communicating clearly and promptly, and cooperating to ensure a smooth transition.

Transfer of documents

Your new accountant must access your financial records to provide accurate and effective services. This typically includes:

- Tax returns: Previous years’ tax returns to understand your tax history.

- Financial statements: Balance sheets, profit and loss statements, and cash flow statements.

- Business activity statements (BAS): Records of GST, PAYG withholding, and other tax obligations.

- Supporting documentation: Invoices, receipts, bank statements, and other relevant financial records.

Your new accountant will usually request these documents directly from your old accountant, streamlining the process for you.

Client authorisation

To initiate the transfer of your financial information, you’ll need to sign an authorisation form. This form grants your existing accountant permission to release your records to your new accountant, a key step when you feel changing accountant.

This process is not only crucial for maintaining tax compliance but also ensures the legal and ethical transfer of your confidential data. It is highly recommended that this transition be managed by a local team of business accounting services known for good service.

Engaging with accountancy services that understand the accounting profession deeply can provide essential business advice as your business grows and maintains its financial health. Additionally, receiving tax advice from trusted service providers within the accounting business ensures that your needs are comprehensively addressed.

Confidentiality

Understandably, you may be concerned about your financial information’s confidentiality during the handover when you change accountant. Both your old and new business accountants are bound by strict confidentiality agreements and professional ethics to protect your data. You can have a clearance letter signed to keep your confidentiality intact.

As part of the professional clearance process, they will handle your financial information with the utmost care and security, ensuring it remains private and protected throughout the transition. This is especially crucial for a small business or limited company, where financial discretion is key. Its highly recommended using accounting services that uphold these standards to support your business continuity.

Switch to better financial management today

Ready to switch accountants? With Sleek.com, it’s a straightforward process that empowers Aussie businesses to maximize their financial potential. Discover the benefits of great service and professional advice tailored specifically to your needs. If you’re seeking professional guidance that navigates complex tax regulations and offers practical tax tips, look no further.

Our financial services ensure your financial data is handled with precision. Switching accountants might just be a great idea to enhance your business’s financial health. Visit Sleek today and take control of your financial future with confidence.

Conclusion

Knowing how to switch accountants effectively puts you back in the driver’s seat of your business’s financial journey. By finding an accountant who aligns with your goals and proactively supports your growth, you are better positioned for future success. While it may feel like a big decision, a seamless handover to an accountant who’s the right fit can positively impact your peace of mind and bottom line. Remember that a good accountant should provide clear communication, timely responses, and valuable insights to help your business thrive.

FAQs about how to switch accountants

How do I tell my current accountant that I'm switching?

Be professional, honest, and direct. Inform them in writing, express gratitude for their services, and explain your reasons for making the change. Provide a clear timeline for the transition and request their cooperation in transferring necessary documents and information.

Can I switch accountants in the middle of the financial year?

Yes, you can switch accountants at any time during the financial year. However, it’s generally easier to transition at the end of the financial year or quarter to maintain continuity in your financial reporting and avoid potential issues with tax deadlines.

How do I transfer my financial information to my new accountant?

Gather all relevant financial documents, including tax returns, financial statements, payroll records, and receipts. Notify your current accountant of the change and request that they transfer these documents to your new accountant. You may need to provide written authorization for the transfer of information.

What should I look for when choosing a new accountant?

Consider factors such as their experience in your industry, range of services, communication style, and technological capabilities. Look for an accountant who is proactive and responsive and can provide valuable insights to help your business grow. Don’t forget to compare fees and pricing structures to ensure you’re getting good value for money.

How long does it take to switch accountants?

The time required to switch accountants varies depending on your financial situation’s complexity and your previous accountant’s cooperation. Generally, the process can take anywhere from a few weeks to a couple of months. Start the transition process early to ensure a smooth changeover without disrupting your business operations.

Will switching accountants affect my BAS or tax lodgments?

Switching accountants should not affect your BAS or tax lodgments, as long as the transition is well-coordinated and all necessary information is transferred to your new accountant promptly. Be sure to discuss any upcoming deadlines with your new accountant to ensure they are prepared to meet them.

450,000

businesses worldwide.

from 4,100+ reviews.

satisfaction rate from

16,000 surveyed clients.